Trending

The Fed removed its handcuffs on banks, allowing them greater flexibility to trade and hold crypto assets. Before Thursday’s action, banks were asked to seek advance approval from the regulators before participating in crypto-related activities. Further, the Fed removed guidance that banks exercise caution with crypto due to its volatility, liquidity, and legal uncertainty.

The Federal Reserve Board on Thursday announced the withdrawal of guidance for banks related to their crypto-asset and dollar token activities and related changes to its expectations for these activities. These actions ensure the Board’s expectations remain aligned with evolving risks and further support innovation in the banking system.

The Fed’s move should help ease Powell’s troubled relationship with Trump. It may further explain why Trump reversed his stance on firing Powell. Trump has been pushing a pro-crypto agenda. Thus, allowing banks easier access to trade and hold cryptocurrencies will go a long way toward satisfying his wishes.

Market Trading Update

Last week, we discussed the issue with the spat between President Trump and the Federal Reserve chairman, Jerome Powell. As noted then:

“While the markets await the next Federal Reserve meeting, the uncertainty over monetary policy weighs on markets as much as the uncertainty about tariffs. This past week, the market reversed some of its gains from the massive “tariff reprieve” surge. With the MACD back on a buy signal and money flows turning positive, buyers are tepidly stepping back into the market. The 20-DMA continues to act as overhead resistance, defining the current downtrend. While there is undoubtedly a risk of another test of recent lows, which should be expected and why caution remains advisable, a break above the 20-DMA would lead to a rally to the 50-DMA. (Monday’s article addressed the “Death Cross” and what it means for investors.)“

The market rallied above the 20-DMA this past week as investors found some “silver linings” to the ongoing tariff dispute. Despite China saying “no negotiations” had started with the U.S., comments from both President Trump and Scott Bessent suggested that the Administration would “be nice” to China and that a “very good deal” could be done between the two countries. As we have noted previously, given the more extreme oversold condition of the market, any “good news” would allow investors to push stocks higher.

As stated, the market cleared initial resistance at the 20-DMA, but there is a heavy band of resistance just ahead at the level where the market was trying to bottom ahead of the tariff announcements. Just above that is the confluence of the 50- and 200-DMAs. While markets are not overbought yet, sellers will likely re-emerge if the market pushes further into those resistance levels. As we have suggested over the last two weeks, we are likely in for a rather protracted consolidation action as the market digests ongoing trade negotiations, slower economic growth, and reduced earnings expectations. Therefore, we should expect continued pullbacks and rallies until the market resolves the seller imbalances.

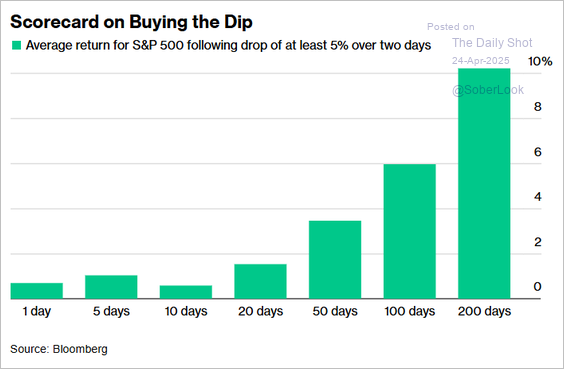

What is very interesting about the recent market decline is that while professional and “older investors,” who are presumably more experienced, are very “bearish” about their investment outlook, retail investors have been “buying the dip” at the most on record going back to early 2023.

However, while you may shake your head in disbelief, buying markets when they are down has been an essentially winning strategy for dip buyers over the last decade. Of course, such should be unsurprising given repeated rounds of monetary and fiscal interventions. As previously discussed, the Fed has engendered an entire generation of young investors with a sense of “moral hazard.” To wit:

“From a market perspective, the liquidity flows from the Federal Reserve increased speculative appetites and investors piled into “zombies” with reckless abandon. Why? Because of a lack of incentive to guard against risk as investors believe the Fed is protecting them from the consequences of risk. In other words, the Fed has “insured them” against potential losses.”

Will this time be different? Maybe. There will be a point where taking on excessive speculative risk in leveraged ETFs and options leads to poor outcomes. However, that may not be today. As such, we need to be mindful that buyers and sellers drive markets. Until the markets change investors’ speculative attitudes, we will likely continue to find support in markets even though we may think there shouldn’t be.

The Week Ahead

Earnings kick into full gear this week, with the most prominent companies reporting. Accordingly, earnings, revenues, and, perhaps most importantly, forward guidance will help steer the market this week. Microsoft and Meta will headline earnings on Wednesday, followed by Apple, Amazon, and Eli Lilly on Thursday. Moreover, there will be reports from companies such as Exxon, Chevron, McDonald’s, Mastercard, Visa, and Coca-Cola.

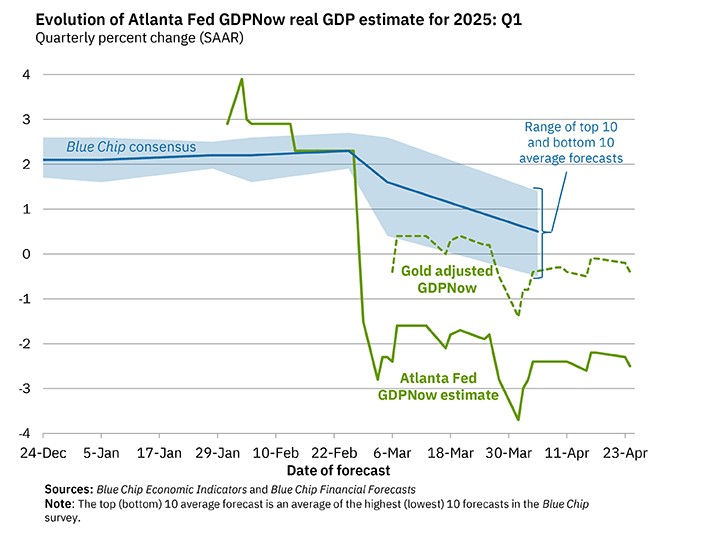

Data on the labor market, inflation, and the economy will be released this week. JOLTS, ADP, and the BLS will update us on the state of the labor markets on Tuesday, Wednesday, and Friday, respectively. Any weakness may provide rationale for the Fed to cut sooner rather than later. Furthermore, GDP and PCE prices will inform the Fed on the state of the economy and prices on Wednesday. The graph below shows that the Atlanta Fed GDPNow forecasts that the economy may have contracted by 2.5%. However, the Wall Street consensus remains slightly positive.

Last week, the Fed was all over the map, from Powell’s more hawkish tone to talk of a June rate cut by other Fed members. The Fed seems confused about the impact of tariffs on inflation. At the same time, they worry the economy is slowing and unemployment is rising, but they have little data to substantiate that claim. Accordingly, they appear handcuffed. Unfortunately, we won’t get much insight from Fed speakers this week as they enter their media blackout before next week’s FOMC meeting.

Speculator Or Investor? 10 Rules From Legendary Investors

Are you a “speculator” or an “investor”? This is an essential question that every individual deploying capital into the financial markets must answer. The reason is that how you answer that question determines how you should behave during market cycles. Over the last 15 years, due to repeated rounds of monetary and fiscal interventions, most investors are simply chasing performance. However, why would you NOT expect this to happen when financial advisers, the mainstream media, and Wall Street continually press the idea that investors “must beat” some random benchmark index from one year to the next?

However, if you are only chasing performance, are you an “investor” or a “speculator”

While some may hold a negative connotation of being called a “speculator,” that would be incorrect. However, it is critical to understand the difference, as being a “speculator” in financial markets requires a different set of “rules” than being an “investor.”

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”