Written by: Kunal Shah and Tatiana Esipovich | iCapital Network

The secondary private equity market comprises the buying and selling of preexisting investor commitments to private market funds. Secondary funds (secondaries) purchase these existing commitments from limited partners (LPs) seeking to exit primary private equity funds before they are fully liquidated. In recent years, the secondaries segment has grown and matured, and may offer significant appeal to investors.

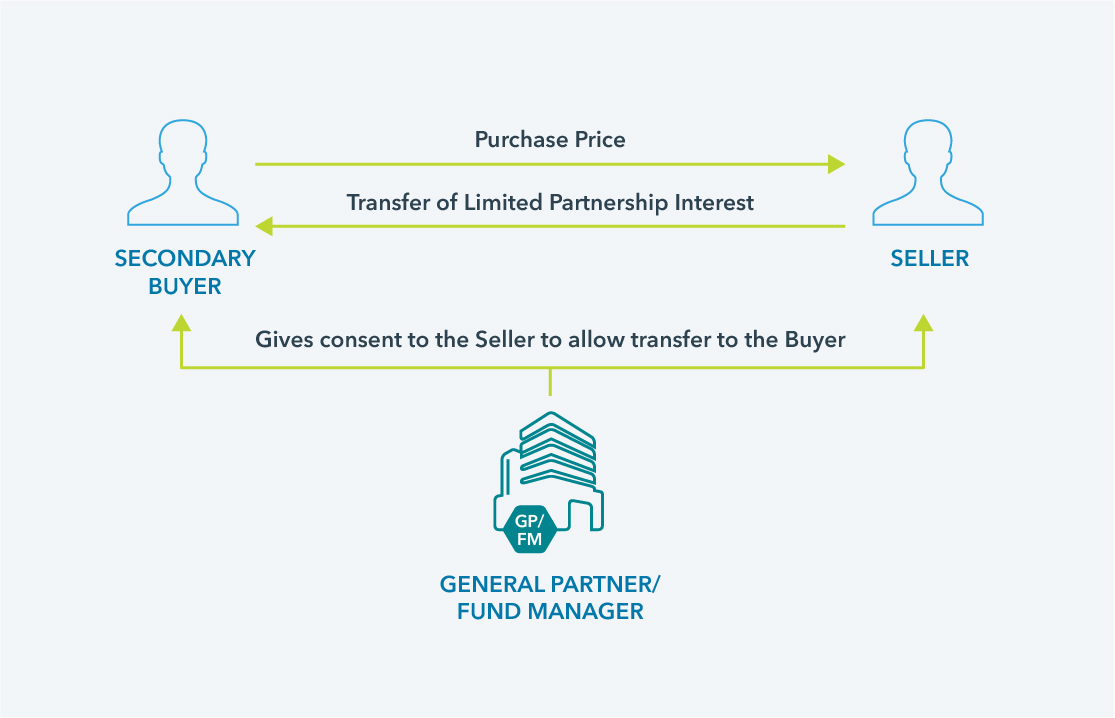

Exhibit 1: An Overview of Secondary Transactions and Participants

Source: Capital Dynamics. For illustrative purposes only.

An accessible entry point into private markets

Secondaries offer several potential benefits for investors and may represent a particularly attractive entry point relative to primary private equity funds because of their unique risk and return characteristics.

Diversification: Secondary funds are typically more diversified than primary private equity funds (such as growth equity or buyout funds) because they assume preexisting commitments in multiple funds. As such, secondary funds may offer significant diversification across managers, industries, geographies, strategies, and vintage years. This diversified approach has the benefit of offering private equity exposure with less risk compared to an investment in a single primary private equity fund.

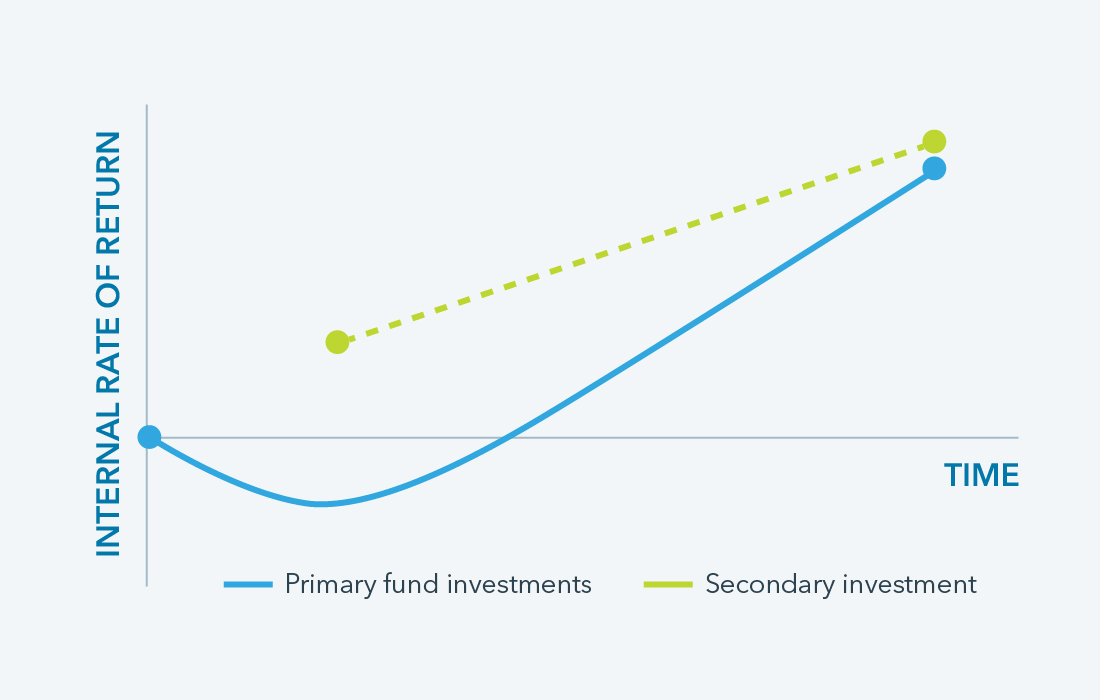

Shorter duration and faster return of capital (mitigated J-curve): In primary private equity funds, it typically takes five to six years to deploy capital, and it can be several years before investors start receiving distributions. By contrast, secondary strategies deploy capital faster and distributions typically begin quickly – in some cases as soon as the fund’s inception – because they are investing in mature underlying funds. This mitigates the private equity J-curve, in which primary private equity funds typically have “negative” returns in the first few years (as investors have to pay management fees and initial investment costs from day one), that then turn into positive returns as the underlying investments mature and start to generate returns that may significantly outweigh the fees and expenses. Exhibit 2 illustrates the typical return profile of a primary private equity fund versus a secondary fund.

Exhibit 2: Typical Return Patterns of Primary and Secondary Private Equity Funds

Source: iCapital Network. For illustrative purposes only.

Discounted access to private equity funds: The ability to exit private equity funds early has historically come at a price to sellers – secondary fund managers would buy preexisting interests in funds at a discount to their net asset value (NAV). As the market grew more competitive in recent years, that discount declined (in 2019, however, secondary portfolios still traded at an average of 93% of NAV1). Secondary investors would benefit immediately from this discount as well as any value creation that takes place subsequent to the investment.

Limited blind pool risk: Investors in primary funds don’t know in advance what investments the fund manager will make. This is known as blind pool risk. Secondaries mitigate blind pool risk by investing in existing commitments. In other words, they know which assets they are acquiring before they invest, enhancing the potential for due diligence and providing visibility into potential future performance.

The state of the market: challenges and opportunities

One upside of the recent market volatility is that pricing levels in the secondary market are expected to potentially adjust downward, leading to a more attractive buying opportunity for secondary fund managers. The secondary market was previously trading at all-time high levels, with large buyout funds being sold at a record-high 100% of NAV.1 These elevated pricing levels were leading to compressed return expectations.

Going forward, a downturn-driven reset will instead see the secondary market readjust to lower valuation levels, enabling secondary fund managers to purchase positions at greater discounts. In all market environments, those managers who succeed in identifying assets outside of competitive auctions or in proprietary situations — or where they benefit from an information advantage — are likely to outperform.

Another element for investors to consider is that, while secondaries can provide a mitigated J-curve and faster return of capital, the cash flow profile of secondary funds is reliant on distributions. If distributions slow (as they might in today’s recessionary market environment), return profiles could lower. Therefore, it is important to select disciplined managers who are keenly focused on downside protection and have a proven track record in navigating market cycles.

For high net worth investors, the secondary private equity market offers several potential unique portfolio benefits. For investors seeking to gain private equity exposure through a primary fund but concerned about the duration or significant gap between making a commitment and receiving distributions, secondary funds may be an attractive option. As with any private equity investment, manager selection is critical to realize the benefits of these strategies.