Trending

The yellow metal may benefit from a prolonged crisis

While the 2011 analog paints an optimistic portrait for gold, silver and mining stocks, a re-enactment of the last debacle is unlikely to unfold this time around. Back then, gold soared amid the debt ceiling chaos, while the USD Index was a major casualty. And while it’s possible lawmakers could ignite a similar event, most learn from their past mistakes.

For example, while bloated stock valuations were the Black Swan in 2000, the 2008 global financial crisis (GFC) was a housing market phenomenon, while the 2020 pandemic was a health scare. As a result, different catalysts often cause distress, and when this recession arrives, it will likely be driven by something investors least expect.

So, with the debt ceiling drama highly anticipated, it reduces the odds of the event unfolding in line with investors’ expectations. Therefore, it’s likely more semblance than substance, and the bulk of the PMs’ rallies should be in the rearview.

Here Comes the USD Index

As evidence, the USD Index has suffered recently, and there are concerns that the ECB could out-hawk the Fed. Well, the reality is that the EUR/USD has largely benefited from a resilient U.S. stock market and low volatility.

Please see below:

To explain, the green line above tracks the daily movement of the EUR/USD, while the black line above tracks the inverted (down means up) daily movement of the Cboe Volatility Index (VIX).

If you analyze the relationship, you can see that the currency pair has moved opposite the VIX for nearly a year. Moreover, when the VIX falls and risk-on sentiment reigns, currencies like the euro rally at the expense of the U.S. dollar. However, the environment should flip as we move forward. We wrote on Apr. 21:

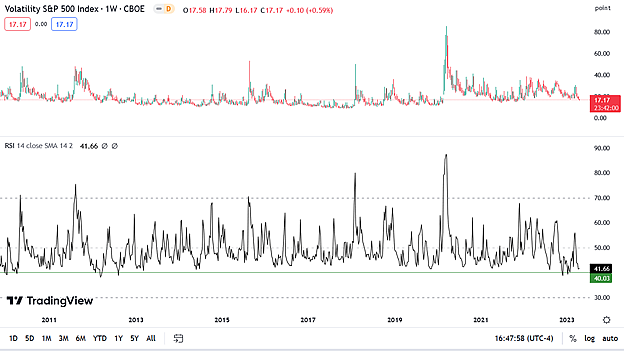

To explain, the candlesticks above track the weekly movement of the VIX, while the black line at the bottom tracks its weekly RSI. If you analyze the horizontal green line, you can see that weekly VIX RSI readings below 40 are rare over the last 10+ years.

We added:

To explain, the blue line above shows how the VIX often bottoms near the end of April, then rises in May, falls again, then hits a new high in June. So, with the VIX’s clock turning bullish after next week, coupled with the rare weekly RSI reading, the data supports more uncertainty.

Thus, while the VIX declined dramatically on Apr. 27, the seasonal weakness is normal. Likewise, its weekly RSI did not make a new, and the shallow reading near 40 highlights how complacency should haunt the bulls in May and June.

To that point, the USD Index showcases seasonal strength in May and July.

Please see below:

To explain, the blue line above shows how it’s perfectly normal for the USD Index to bottom at the end of April. Then, a sharp rally often follows in early May, followed by a pullback, then another breakout to new highs. Therefore, while the crowd assumes April’s winners will maintain their outperformance, if the VIX and the USD Index jump, the PMs’ trends should turn bearish.

Finally, while investors assume that rate cuts are on the horizon, the data suggests otherwise. Despite inflation fatigue causing investors to ignore the ramifications, the pricing pressures remain problematic and the year-over-year (YoY) base effects end in June. As a result, the month-over-month (MoM) readings will matter more, and the implications are far from priced in.

Please see below:

To explain, the Cleveland Fed expects the headline CPI to increase by 0.61% MoM in April, which, if realized, would be the highest MoM reading since June 2022. And while the Cleveland Fed has been off on its headline CPI predictions, its core CPI estimates have been accurate. As such, 0.46% MoM annualizes to 5.66% YoY, and a continuation of the theme will look even worse after June.

Overall, we believe the Fed’s tightening cycle has more room to run, and a realization is bullish for the USD Index and real interest rates. In addition, we’re days away from the calendar turning bullish for the greenback, and with risk assets rallying in April, investors loosened financial conditions, which uplifts inflation. Thus, don’t be surprised if the narrative shifts dramatically in the months ahead.

Will April’s winners suffer in May and June, or will their bullish trends continue?

Related: Could Stagflation Save Gold In 2023?